Stamp Duty Land Tax (SDLT) Rates

Stamp Duty is a tax you pay on property purchases. The rate of tax you pay is a percentage of the property selling price. But it’s not just a simple percentage, rates of stamp duty increase over different thresholds.

Here are the current Stamp Duty Land Tax rates for England, Wales and Northern Ireland in a fancy little table:

| Purchase price | Residential SDLT rates | Additional property rates* |

|---|---|---|

| 0* to £125,000 | 0% | 3% |

| Over £125,001 to £250,000 | 2% | 5% |

| Over £250,001 to £925,000 | 5% | 8% |

| Over £925,001 to £1.5 million | 10% | 13% |

| Over £1.5+ million | 12% | 15% |

| *Transactions under £40,000 do not require a tax return to be filed with HMRC and are not subject to the higher rates. | ||

Examples

If you buy a house for £300,000, the Stamp Duty you owe is calculated as follows:

- 0% on the first £125,000 = £0

- 2% on the next £125,000 = £2,500

- 5% on the final £50,000 = £2,500

- Total SDLT = £5,000

If you already own a property and you’re buying an additional property for £300,000, the Stamp Duty you owe is calculated as follows:

- 3% on the first £125,000 = £3,750

- 5% on the next £125,000 = £6,250

- 8% on the final £50,000 = £4,000

- Total SDLT = £14,000

Use our Stamp Duty Calculator to work out how much tax you’ll pay:

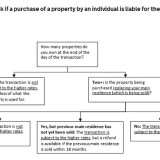

Replacing Your Main Residence

If the property you’re buying is replacing your main residence (maybe you’re moving home) and your current residence is sold, you DON’T pay the extra 3% Stamp Duty.

But if there’s a delay in selling your current residence and you still own it after completing your new property purchase, you DO pay the higher rate (because you own 2 properties).

If you sell your previous home within 36 months, you can get a refund on the higher rate Stamp Duty you paid. You can apply for a repayment of the higher rates for additional properties online, click here.

Example Scenarios

HMRC produced an updated SDLT Guidance Note in November(2016), which include these sample scenarios:

The higher rates will not apply to the joint purchase by Mr and Mrs S of a new main residence. As they are married and have both lived in the property owned by Mrs S as their main residence they will both be treated as replacing their main residence.

The higher rates will apply to the joint purchase of a new main residence by Mr P and Ms B. As they are not married (or in a civil partnership) Mr P will not be treated as replacing his main residence as, even though he has been living in the property owned by Ms B, he has no interest in the property Ms B is selling.

Example 3 – new main residence

The higher rates will apply to the purchase of the new property as following the purchase Mr T will own an additional residential property and is not replacing his main residence. Mr T will not be able to claim a refund when he sells his current buy-to-let property as refunds are only available where a previous main residence has been replaced.

Ms G will be treated as replacing her main residence if the property she sold six months ago was her only or main residence and completion occurred on or before 26 November 2018. The fact that she lived in one of her buy-to-let properties in the interim period does not affect this.

Example 5 – mixed use property

The higher rates will apply to the purchase by Mr and Mrs C as they already own an interest in another residential property: the flat above the shop.

The higher rates will apply, as Ms D will be purchasing a major interest in a property, is not replacing her main residence and owns an interest in another property.

Example 7 – buy-to-let and 50% share

The higher rates will apply as Miss L is purchasing a major interest in a residential property, is not replacing her main residence and owns an interest in another residential property.

Example 8 – gifted a half share

The higher rates will not apply if no consideration of any kind is given for the property. However, if Ms W took over responsibility for half of the outstanding mortgage on the property this would count as consideration and the higher rates would apply. Further guidance on this is available on GOV.UK at https://www.gov.uk/guidance/sdlttransferringownership-of-land-or-property#if-you-transfer-property-because-of-divorceseparation-orthe-end-of-a-civil-partnership.

Example 9 – gifted a half-share

The higher rates will apply to the purchase of the new property as Mr F already owns an interest in another residential property and is not replacing his main residence.

Example 10 – transferring 50% of a buy-to-let

The higher rates will apply to the transfer as Mr I owns other residential properties. As a married couple other residential property owned by either spouse is taken in account in determining whether the higher rates apply.

Example 11 – transferring equity to wife

The higher rates will apply as Mrs X owns an interest in another residential property and is not replacing her main residence. The higher rates will apply to the value of the mortgage taken over by Mrs X.

Example 12 – buy to merge two properties

The higher rates will apply as following the purchase Ms Q will own an additional residential property and is not replacing her main residence. A refund of the higher rates cannot be claimed once the work to merge the two properties is complete as refunds are only available where a previous main residence has been replaced.

Example 13 – extending the lease

The higher rates will apply as Mr E is purchasing a major interest in a residential property, owns an interest in another residential property and is not replacing his main residence.

The higher rates will apply to the purchase of the second buy-to-let property as following the purchase Mr B will own an additional residential property and is not replacing his main residence. A refund will not be available if Mr K subsequently sells one of his buy-to-let properties as a refund is only available where a main residence has been replaced.

Example 15 – increasing share in a shared ownership

As Ms R owns another residential property the higher rates will apply to the purchase of the additional share in the property subject to the statutory shared ownership arrangement unless the replacement of only or main residence exception applies.

Example 16 – armed forces personnel stationed overseas

The higher rates will apply to the purchase by Mr N of the new property even if he sells one of his rented properties, as neither has been his main residence. The SDLT rules do not allow armed forces personnel to treat a dwelling that they have never lived in as their main residence.

Example 17 – property builders

Although there are no specific reliefs from the higher rates for property companies, other SDLT reliefs will still be available including those in Schedule 6A of the Finance Act 2003, provided the conditions for the relief are met.

Example 18 – inherited 50% share

The higher rates will not apply to the purchase of the new property by Mr A provided that this is purchased within 3 years of inheriting the property, and during that 3 year period the interest held by Mr A in the inherited property, together with any interest held by his spouse or civil partner, does not exceed 50%.

Example 19 – helping son buy his first property

Example 20 – buying property with a annexe

For the purposes of the SDLT higher rates, the house and annexe would be treated as a single dwelling. As Mr and Mrs Z own no other residential property the higher rates will not apply.

Example 20 – buying property with a annexe

For the purposes of the SDLT higher rates, the house and annexe would be treated as a single dwelling. As Mr and Mrs Z own no other residential property the higher rates will not apply.

Example 21 – new main residence

its garden being valued at £150,000.

As the cottage is in the grounds of the main house and worth less than a third of the total purchase price, for the purposes of the higher rates Mr Y may claim multiple dwellings relief and will be treated as purchasing only one property. As he is replacing his main residence the higher rates will not apply.

As the barns are worth more than one third of the total purchase price Ms V will be treated as purchasing four properties. As she already owns another residential property and is not replacing her main residence the higher rates will apply, although multiple dwellings relief may be claimed.

Example 23 – before 26 November 2015

Transitional provisions provide that where a contract was entered into before 26 November 2015 but is not completed until on or after 1 April 2016, the higher rates do not apply provided the contract is not varied after that date. As the contract was varied in May 2016 the transitional provisions will not apply and, as Mr B owns other residential property, the higher rates will be due on completion of the purchase.

Provided Miss M purchases her new main residence on or before 26 November 2018, and has not acquired another main residence in the interim period, she will be treated as replacing her main residence and the higher rates will not apply.